You have likely seen the market go parabolic, watched the funding rates on your favorite exchange climb into the double digits, and wondered if there was a way to capture those fees without getting wiped out by a sudden reversal. We have all been there. It is the classic “siren song” of the crypto markets: the promise of high, seemingly “risk-free” yield just by clicking a few buttons. But if you are simply chasing the highest percentage, you are setting yourself up for a classic trap.

The secret isn’t just about finding a high rate; it is about building a “delta-neutral” fortress around your capital. By using a strategy known as funding rate arbitrage, you can theoretically strip away the volatility of the crypto market and turn your portfolio into a high-yield interest-bearing machine. Let’s break down how this works and, more importantly, how you can execute it without losing your shirt.

Decoding the Mechanics of the “Carry Trade”

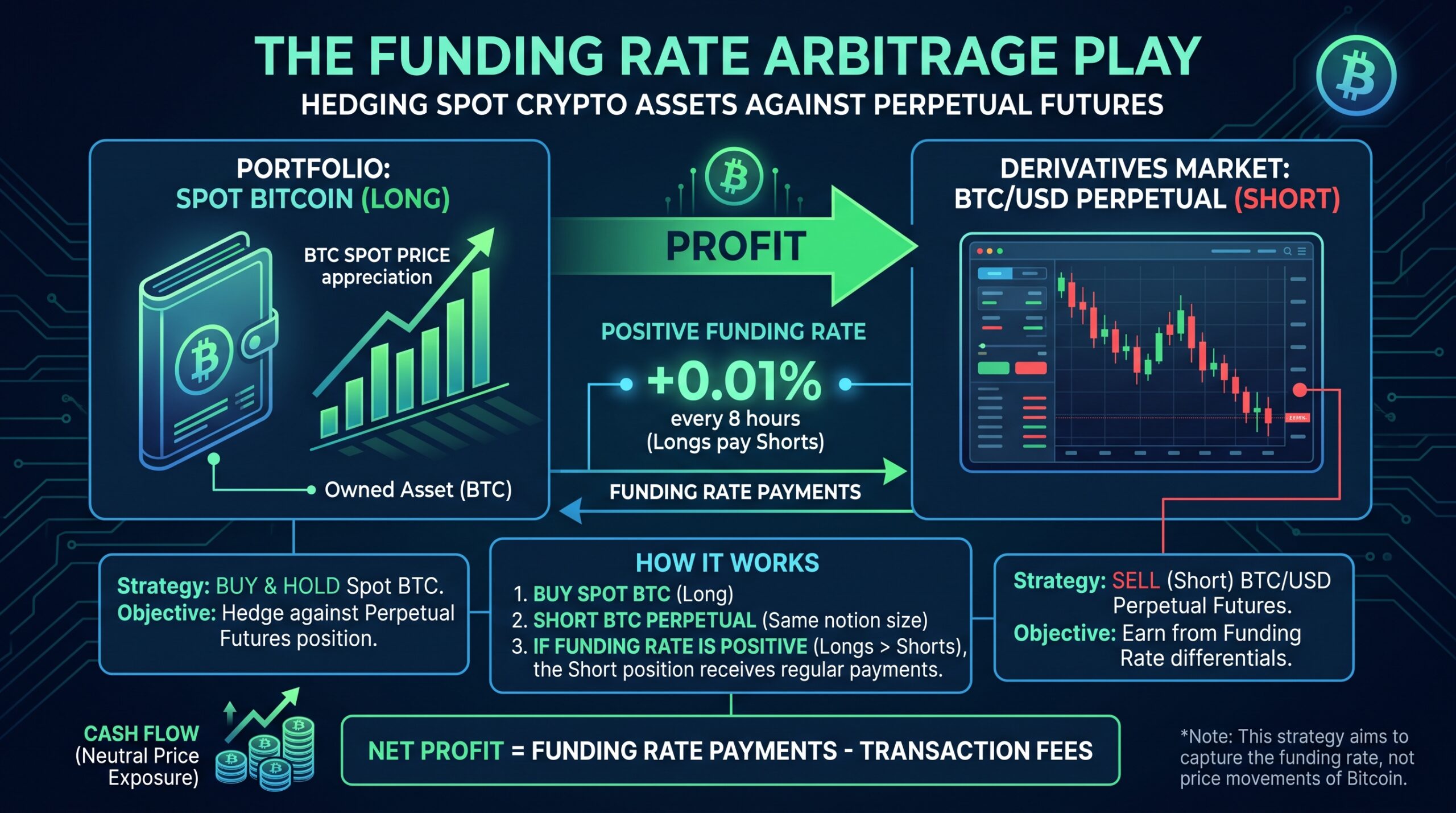

At its core, funding rate arbitrage—often called the “Cash and Carry” trade—is about exploiting the difference between the spot price of an asset and the price of its perpetual futures contract. When perpetual contracts trade at a premium to the spot price, the funding rate is typically positive. This means that those who are “long” the futures pay a fee to those who are “short.”

Expert Insight: As an arbitrageur, your goal is to be the one receiving that fee. You do this by going long on the physical asset (the spot market) and simultaneously shorting the exact same amount in the perpetual futures market. Because your long and short positions are equal, you are “delta-neutral”—meaning the rise or fall of the coin’s price has almost zero impact on your balance. You are literally betting that the price will stay the same, while you pocket the premium.

Why the Market “Pays” You to Hedge

New traders often ask, “Why would the market give me free money?” The answer is simple: stability. Perpetual futures don’t have an expiration date, so the funding rate is the “tether” that keeps the futures price from drifting too far away from the actual spot price. When too many people get bullish and leverage up on long positions, the funding rate rises to incentivize shorts, which brings the price back down. You aren’t getting “free” money; you are being paid a premium by the market for providing the liquidity that keeps the system stable.

Personal Example: I remember a bull cycle where BTC funding rates stayed at 0.05% every eight hours. It sounded small, but that’s 15% APR on my capital with near-zero directional risk. I didn’t care if Bitcoin went to $100k or $50k. As long as the funding stayed positive, my position grew while others were busy gambling on the direction.

The Triple Threat: Risks You Cannot Ignore

While it sounds like a perfect strategy, funding rate arbitrage is not “risk-free.” The most significant danger is a rate flip. If the market sentiment suddenly turns bearish, the funding rate can switch from positive to negative. Now, instead of receiving fees, you are the one paying them.

-

Basis Risk: Sometimes, the gap between the spot price and the futures price widens or narrows unexpectedly. If you have to exit your hedge while the basis is unfavorable, you could lock in a net loss that wipes out weeks of collected funding fees.

-

Execution Costs: Fees are the silent killer. If your exchange’s trading fees exceed the funding rate you are collecting, your “arbitrage” is actually a net-losing strategy.

-

Liquidation Risk: Even though you are hedged, your short position is still a margin position. If the price of the asset spikes vertically, your short could hit a liquidation point before your spot gain can compensate, especially if you aren’t managing your collateral properly.

Building Your Execution Workflow

Profitable arbitrage requires more than just a spreadsheet; it requires precision. Start by selecting assets with high liquidity and consistent, deep funding rates. Avoid “micro-cap” coins where the spread between buy and sell orders will eat your profits whole.

Expert Insight: The most successful pros don’t just hold the position forever. They look for “funding windows.” They enter the trade shortly before the funding settlement time (often 8 hours or 1 hour depending on the exchange) and assess whether to stay in or exit. If you find a pair with a 0.05% rate, you are capturing that gain and re-evaluating the trade three times a day.

Funding rate arbitrage is a powerful tool for turning market volatility into steady, predictable yield. By neutralizing your directional exposure, you stop being a gambler and start acting like a market maker. Just remember: the market pays you to balance it, but it will punish you if you get greedy or lazy with your risk management. Keep your hedge tight, watch those funding rate flips, and always account for your trading fees.

FAQ

What is “Delta Neutral”?

Delta neutral is a portfolio strategy where the total delta (the sensitivity of your portfolio to the price of the underlying asset) is zero. By holding long spot and short futures of equal value, price changes cancel each other out.

How often do I need to rebalance my position?

This depends on your risk tolerance. Some traders rebalance only when their hedge drifts more than 1-2% due to price action, while others “set and forget” until they choose to exit the trade.

Is this strategy better for bull or bear markets?

This strategy is most profitable in a strong bull market, where bullish sentiment keeps funding rates consistently positive and high.

What happens if the exchange goes down?

Counterparty risk is real. If you are doing this on a single exchange, you are vulnerable to that platform’s solvency. Some advanced traders use “cross-exchange” arbitrage—long spot on one exchange and short futures on another—to diversify this risk.